National Institute on Retirement Security Releases a Study on Retirement Readiness for Working Americans

Study Overview

Earlier this year, the National Institute on Retirement Security released a study focused on Retirement in America. Based on their findings, the average American worker is well below where they need to be for a comfortable retirement.

The report focused mostly on those still working rather than those already retired. The study included workers in both the private and public sectors and included employees covered by Collective Bargaining along those that are not. Since most employees are in the private sector and not covered by a CBA, the results are skewed to that population.

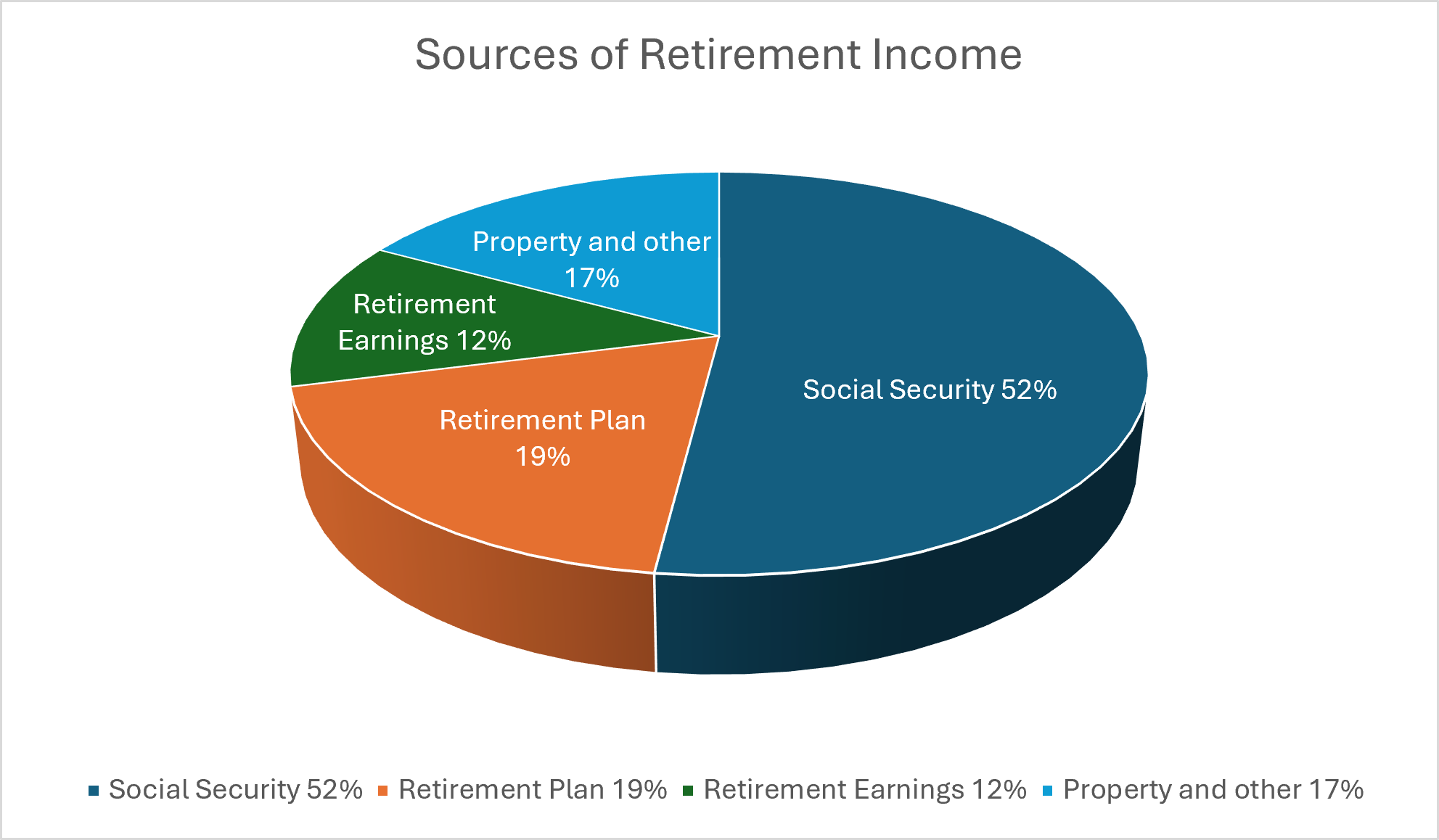

One of the key takeaways from the study is the continued erosion of the “three legged retirement stool” made up of Social Security, employer sponsored retirement plan and personal savings. As you will see in the graph below, Social Security accounts for over 50% of people’s retirement income/savings.

Social Security has been, and hopefully will continue to be, an important part of most retiree’s income. However, the 52% is an indication that the other two sources of retirement income (Employer plans and personal savings) have been declining.

Employer Retirement Plans

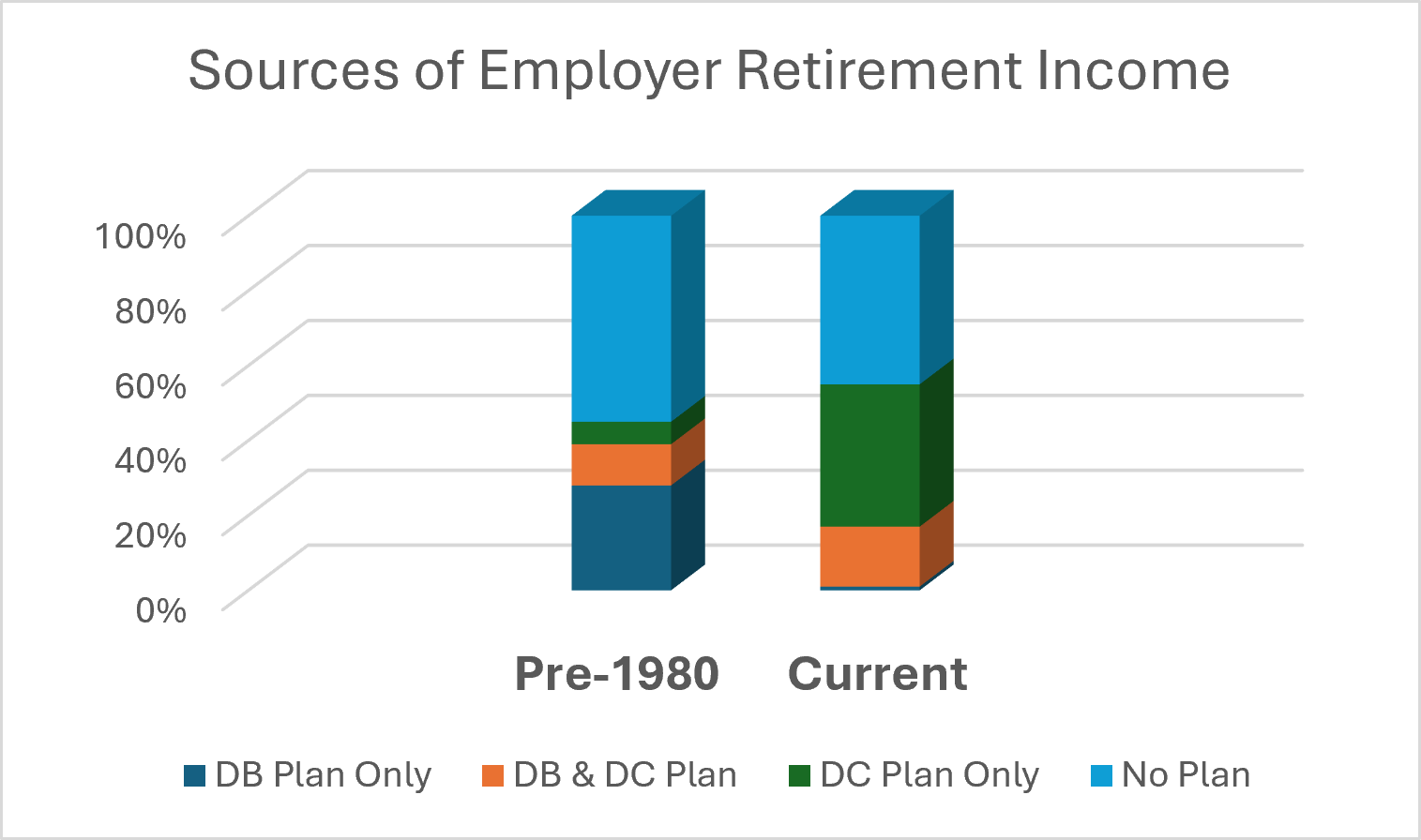

It has been well documented that the private sector has shifted over the last 40+ years from Employer’s providing Defined Benefit Plans to instead providing Defined Contribution Plans as the primary (only, actually) source of Employer sponsored retirement plans.

Currently, only 17% of working Americans have access to a Defined Benefit plan with this largely driven by Union employees in both the private and public sector.

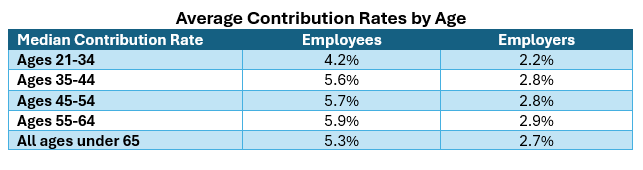

Looking closer at current retirement savings for working Americans, we see the following:

When we look only at those with an employer sponsored retirement savings plan, we see that one half of those have an account value below $40,000. The average of $179,082 does paint a better picture but this is largely driven by very large balances at the higher end, which is why the median amount (1/2 above and ½ below) provides more insight. Further, when we factor in those without a plan (All Working Americans), the median is under $1,000.

These account value results are primarily driven by the amount of contributions made and earnings on those contributions (net of any pre-retirement withdrawals). Below are the current retirement plan savings rates behind these low balances.

Are Americans on Target for Retirement Income?

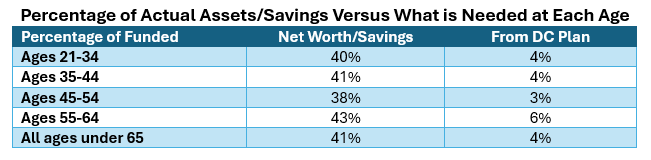

The study also looked at where working Americans are versus how much savings they should have. To do so, they compared how much total savings American workers have as a percentage of what was needed (on average) at their current age. The results are that the average worker has 41% of the retirement assets they should have. For example, if they should have $500,000 in total assets, the typical worker only has $205,000. In addition, their Employer sponsored retirement plan provides just 4% of the 41%.

Please note that these results include those with no DC Plan/Account which is why the 4% is so low. If we only look at those with a Plan, the 4% does improve to 19%.

Conclusion

The study clearly illustrates that most American Workers are not reaching retirement savings benchmarks and went on to suggest several policy based solutions to this retirement shortfall.

Social Security – Since this is 50% or more of retirement income for most Americans, it’s important for Congress to keep the Trust Fund well-funded on an actuarial basis.

Defined Benefit Pension Plans – Much of the underfunding results can be tied back to the significant decline (to the point of extinction) of DB plans in the private non-union sector. Preserving DB plans and increasing availability of pensions are essential to bolstering retirement security.

Defined Contribution Plans – While Congress and some states have taken actions to help improve the DC “system”, as can be seen from this study, gaps and issues remain. In addition, the voluntary design of a 401(k) plan actually creates additional disparity between those with the disposable income to defer/save versus those where deferring any of their current earnings for retirement would result in other immediate financial consequences.

Long-Term Care – While not directly a retirement benefit, the need for and the cost of long-term care can significantly drain retirement savings. Unfortunately, currently there are not many good market based products/options for long-term care. Both individual states and Congress are looking into solutions for long-term care.

The full study is available at www.nirsonline.org/research/retirementinamerica2026/