“I Pay Dead People”: A Trustee’s Nightmare, Why Retiree Verification Is Becoming Essential

As I’m sure we are all aware the primary function of a pension plan is to pay members, when due, the correct lifetime benefit they have earned. One of the recurring concerns is not ceasing payments for retirees or beneficiaries who pass away.

Historically, many pension administrators relied heavily on the Social Security Administration's Death Master File (DMF) to identify deceased participants. The DMF, includes more than 100 million records created from SSA payment records, contains the social security number, name, date of birth, and date of death of each decedent for which the SSA has a record. However, changes enacted in 2013 under the Bipartisan Budget Act restricted public access to the DMF for the first three years after a death is reported. As a result, many pension plans lost timely access to a key source of mortality data and were required to adopt alternative verification methods.

Most plans and administrators now rely on reports developed by specialized search companies. However, most of these search companies rely on public records such as death notices, obituaries, etc. Consequently, they cannot provide the same level of certainty that the DMF database had previously provided. This greatly increases the likelihood of continuing payments after a retiree/beneficiary passes away. In addition, the guardrails/restrictions on recouping overpayments introduced in The SECURE Act, can further complicate recovering overpayments.

Faced with this issue, more and more Defined Benefit plans are adding a Retiree Verification process. These are also commonly referred to as "life verification", "proof of life", or even “are you alive letters”. The approach is to annually have some or all retirees/beneficiaries verify that they are, in fact, still alive.

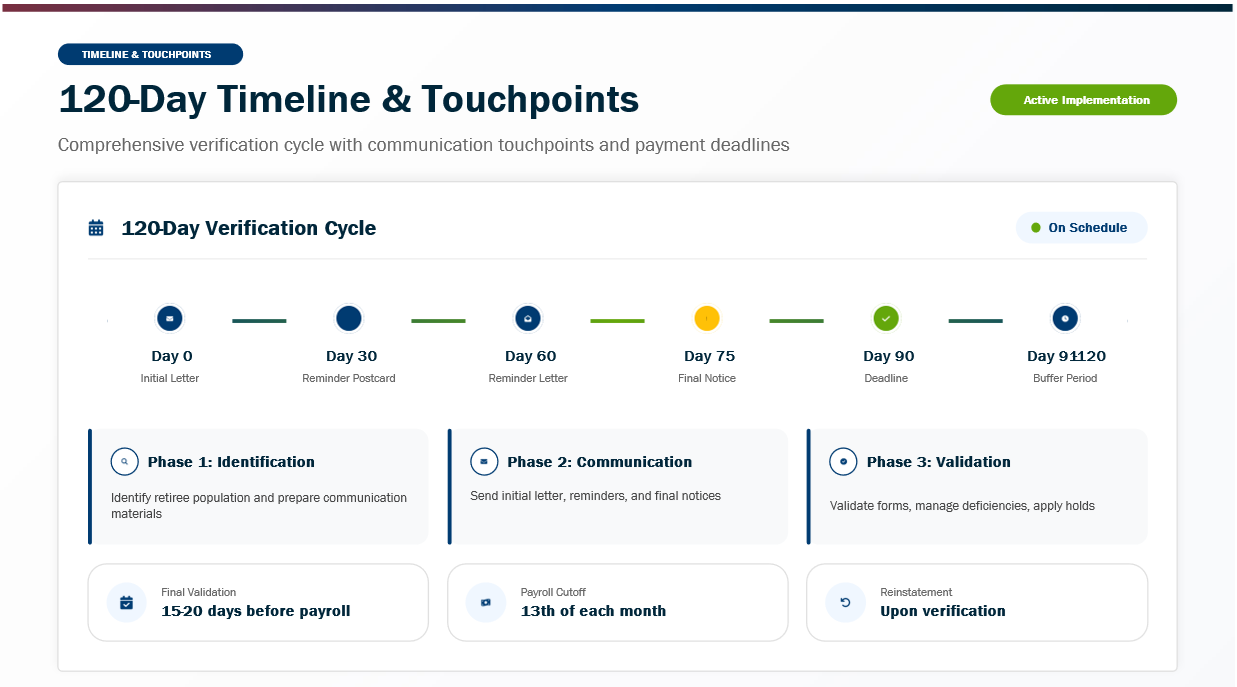

The practice involves a reach out (typically a letter) with a form to be completed, notarized and returned to the plan’s administrator. Plans (and Trustees) must be prepared to withhold payments to those who do not fully respond, therefore it’s important to include ample warnings and time before doing so. Below is what we believe is a best practice for this.

Initial Retiree Verification Mailing - A Retiree Verification form is mailed or electronically delivered to retirees selected for verification. Participants are typically given 30 days to complete and return the form.

First Reminder Notice Sent 30 Days After - If no response is received within the initial period, a reminder note/letter is issued. Retirees are generally provided an additional 30 days to respond.

A Second follow-Up is Sent in 60 Days - For nonresponsive participants, administrators should send a second notice.

A Final Notice is Sent in 75 Days – A third and final notice is sent.

Withhold Monthly Pension (91–120 Days) - When a participant's status remains unverified after multiple attempts, benefit payments should be withheld.

Reinstatement Upon Verification - Once the retiree provides satisfactory proof that they are living, benefits are reinstated. Any withheld payments should be paid retroactively.

While plans are not required to perform this added level of security, we believe it’s a best practice for all Defined Benefit Plans and to that end have developed a very cost effective program for the plans we administer. If you would like more information on this, please contact your Zenith Client Services professional.